New insured mortgage changes are now live, and although I mentioned them in October, they warrant a closer examination.

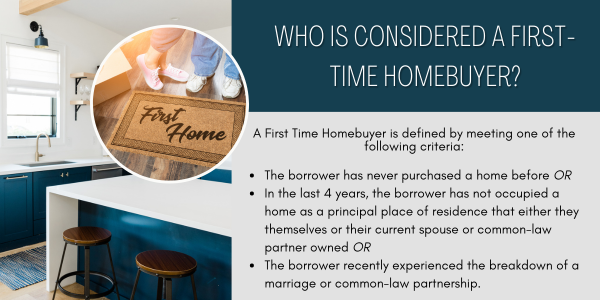

First, What is an Insured Mortgage?

An insured mortgage applies when the borrower has less than a 20% down payment. Lenders require insurance against default, with the borrower paying a premium added to the mortgage.

So What's New?

This month, two significant changes to insured mortgages have officially come into effect. Here’s a quick breakdown:

1. Expanded Eligibility for 30-year Amortizations for First-time Homebuyers (FTHB) and All Buyers of New-Build Properties

While 30-year amortizations for first-time home buyers (FTHB) purchasing new-build properties are already in place, the latest update now extends this option to anyone purchasing a new-build property and FTHB purchasing any owner-occupied property.

With the new changes to insured mortgages, a FTHB earning $75,000 annually can now qualify for about 7.2% more in actual mortgage financing on a 30-year amortization, even with the 20 bps surcharge to the default insurance.

2. Higher Price Caps for ALL Insured Mortgages:

The price cap for insured mortgages has increased from $999,999 to $1,499,999—a significant change our industry has long advocated for. This adjustment is expected to benefit markets where average home prices exceed $1 million, easing the burden on first-time homebuyers who often rely on the "Bank of Mom and Dad" to meet the 20% down payment requirement.

Previously, purchasing a $1.5M home required a $300K down payment. Now, with the recent changes, that same home can be yours with as little as $125K down—provided you meet one critical condition: having the income to support a $1.375M mortgage.

Down Payment Breakdown Remains Unchanged:

5% on the portion up to $500,000

10% on the portion between $500,000 and $1.5 million

Market Impacts:

These changes aim to make it easier for more people to qualify for a mortgage. Here’s how this could impact the market:

Impact on Buyers: A 30-year amortization increases qualifying income, helping some buyers enter the market. Even small changes can boost interest, driving demand and putting upward pressure on home prices. Buying now may offer less competition and better prices before demand pushes values higher.

Selling a Home: If your home is priced between $1M and $1.5M, the recent changes to the price cap have likely expanded the buyer pool. More buyers can now qualify with a smaller down payment for homes over $1 million, potentially leading to higher offers.

If you’re considering buying or selling, now is the time to plan. Reach out to discuss how these changes may impact your goals.

Coming Late January: Insured Refinances for Secondary Suites

The next round of insured changes is on its way, focusing on refinances for secondary suites. Stay tuned—I’ll keep you updated as more details come out in our February issue!

Comments:

Post Your Comment: