Spring is here, and with it comes our beloved Toronto Blue Jays and their ever-loyal commentator, Buck Martinez.

Nothing signals the arrival of spring quite like baseball, with Buck's soothing voice in the background as he announces plays from his broadcast booth, sharing all the insights he gained from observing the players during spring training. But what does Buck have to do with first-time home buyers? Well, just as we welcome another season of baseball, the housing market also welcomes a new wave of enthusiastic first-time home buyers (FTHBs) with thoughts of homeownership on their minds.

There’s no argument it’s more challenging to purchase a home today, but it’s not unachievable. Whether you're looking to buy your first home or you know someone who is, this issue is for you. Let's start with the basics.

Set Realistic Expectations. Set realistic expectations when buying a home. Lower rates in the past made it possible for some first-time homebuyers to skip straight to their "forever" home, but that's not the case anymore. Get comfortable with buying a true first home that may need some TLC, while you build equity for your next home.

What’s your Budget? Consider both what you are “qualified” for and what you can “afford’ when establishing your budget. Account for all expenses, including groceries, child care, insurance, and entertainment, to determine your ideal purchase price. It's important to avoid being "house-poor" when buying your first home.

Understand the 3 Key Factors for Qualifying for a home:

Credit - You need to have two forms of credit, reporting for 2 years with an available credit limit of $2000 on each.

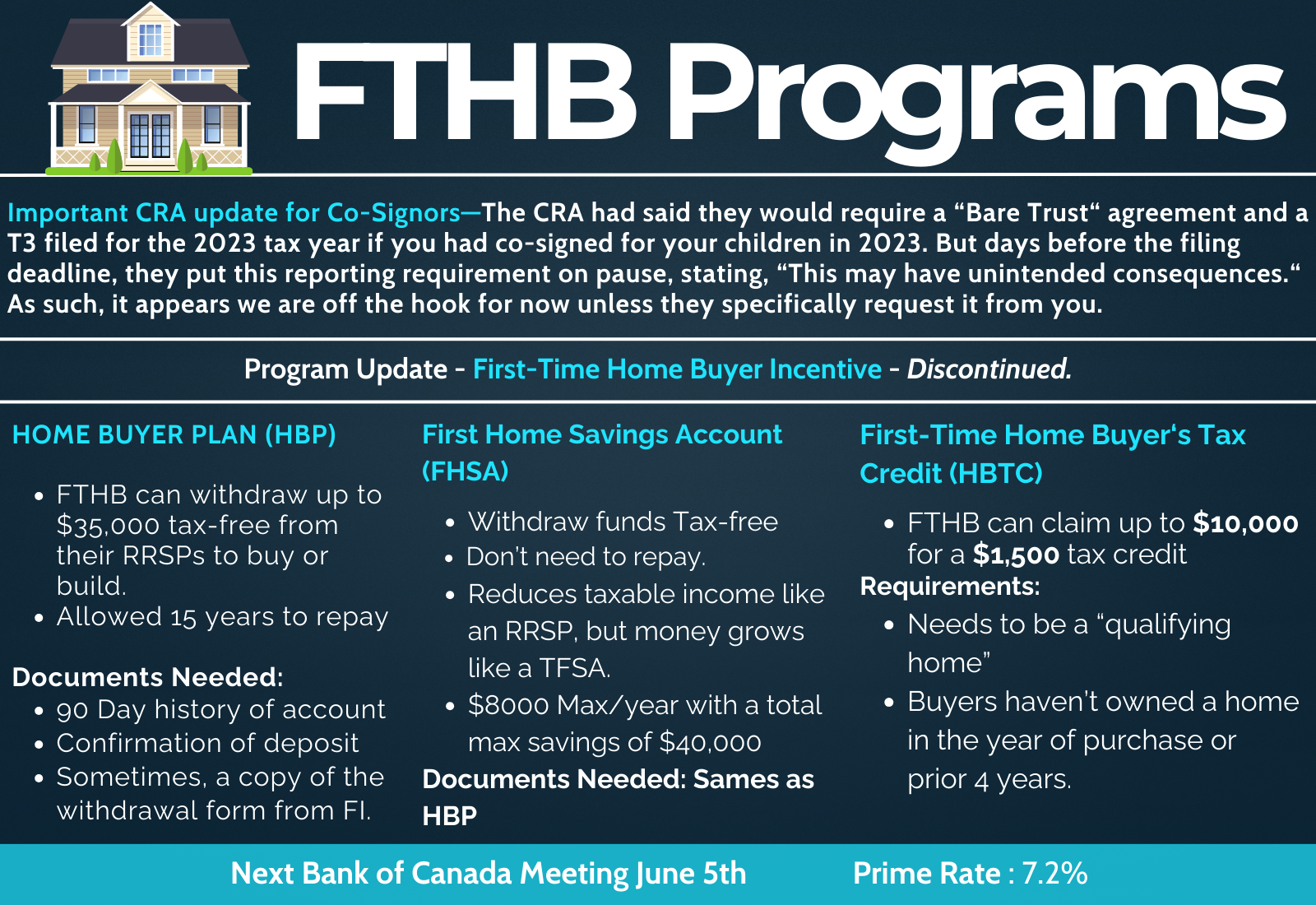

Down Payment and Closing Costs - The general rule is 5% for the first $500k and 10% for the next $499,999. Over one million is 20% down. You need to qualify for your down payment, so if ratios are out, you may need to either increase the down payment or lower the purchase price. ALL lenders require a 90-day history of all accounts your down payment and closing costs are coming from. See the graph below for Down Payment Programs.

Income - Lenders want to see a steady history of employment, ideally two years. The length and documentation required will be based on the type of income. For example, if you want to use hourly income with overtime, we will need two years' T4s. For full-time guaranteed salaried, a letter of employment and a pay stub will suffice. To better understand how your income will be viewed, I can answer this on a call.

Pre-Approved or Pre-Qualified? It's important to understand the difference between getting pre-approved and pre-qualified. Most Realtors require a proper pre-approval before starting the house-hunting process. Unlike pre-qualification, a full pre-approval involves a thorough review of your financial situation, including determining your maximum purchase price, collecting and reviewing all relevant documents, locking in interest rates, and conducting a credit check. If you haven’t had this done, you are only pre-qualified.

Finally, find your tribe. Having a good Realtor and home inspector can make the difference between a smart home purchase and one you will regret. A Realtor will gather all the information you need to know about the market value of your home, neighbourhood specifics, and any market dynamics you need to be aware of. The home inspector will help you ensure that you are aware of any current or future repair needs so you can make an informed decision.

Of course, each of these categories involves many small steps, all of which can be discussed over a call. Despite the widespread message about high rates, the rates for those interested in buying a home have actually decreased significantly. This means that now is a favourable time to make a purchase, as further rate decreases could lead to an increase in home prices once again.

Let's start preparing to buy.

Comments:

Post Your Comment: